A Quantitative Look at Biotech Platforms

While plenty of great writing on platform biotechs has emerged over the years including from our team, we believe the conversation misses a quantitative framing. We sought to precisely answer what successful platforms have tended to look like as they scale.

Our team used a whole lot of GPT Pro tokens to compile clinical, partnerships, and financial data on the 100+ most successful public platform biotechs of all time. We repeated queries until no new info was retrieved and then averaged across 100+ companies so the figures should be at least in the right ballpark. However, they’re likely biased towards overestimates because what’s readily available online is likely biased towards good results. Many failed trials and assets surely fell silently into the dustbins of history. This bias likely gets stronger for older platforms.

Anyways, with that disclaimer out of the way, some of the novel insights from the data dump include:

- Just 16% historically have gone public with an asset later than Phase I

- 25% of the 90 companies' initial lead candidates ultimately got approved

- 50% of the most successful platform biotechs ever ultimately got 1+ drug approved. That means that for 25% of them, it wasn't their lead asset at IPO. To be fair, many companies were pre-clinical, PI or in diagnostics at IPO.

- Just 25% of the most successful platforms ever get multiple drugs approved. 15% get 3+.

- Ownership retained from partnership deal structures typically goes from ~60% for the first two drugs to 80%+ thereafter

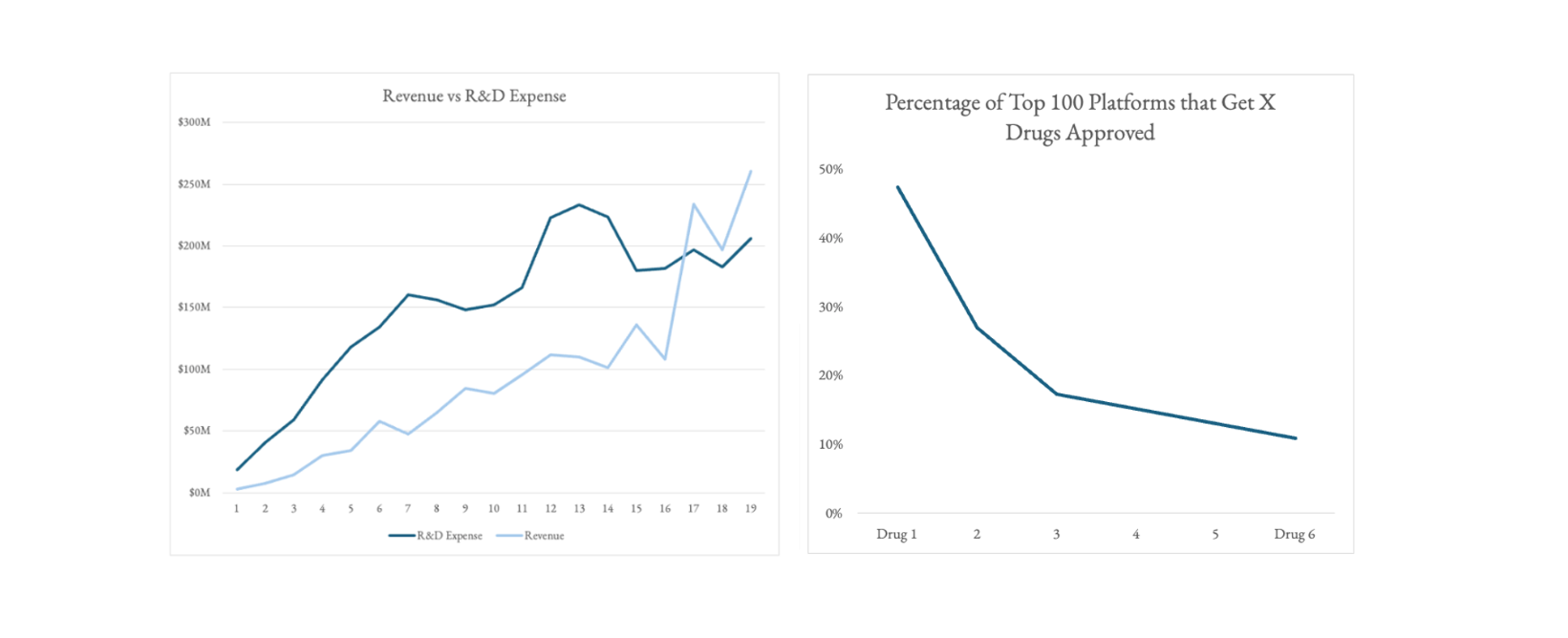

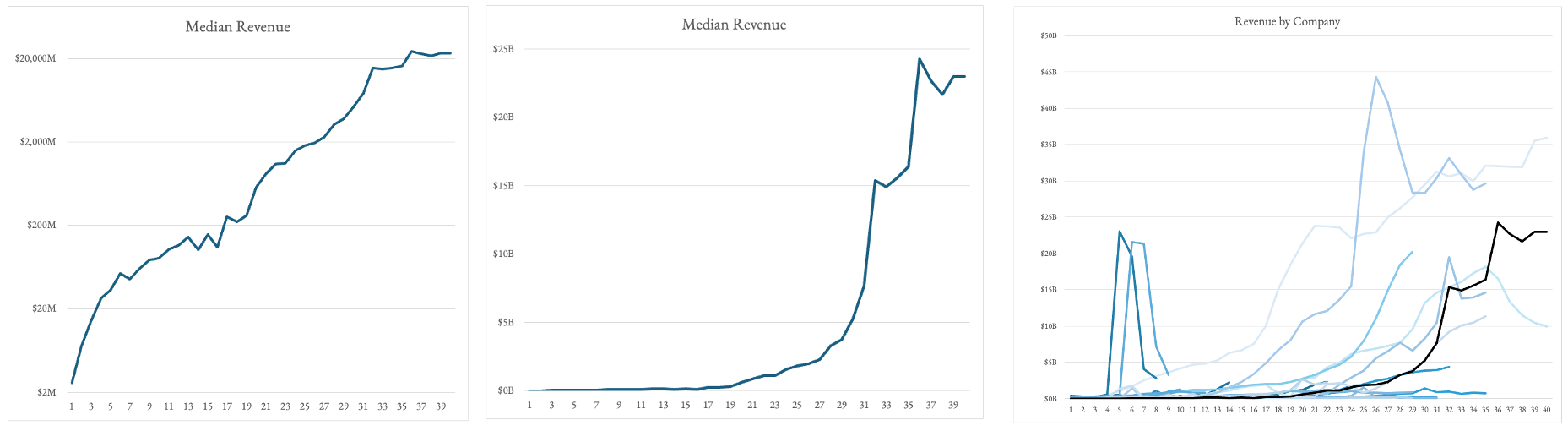

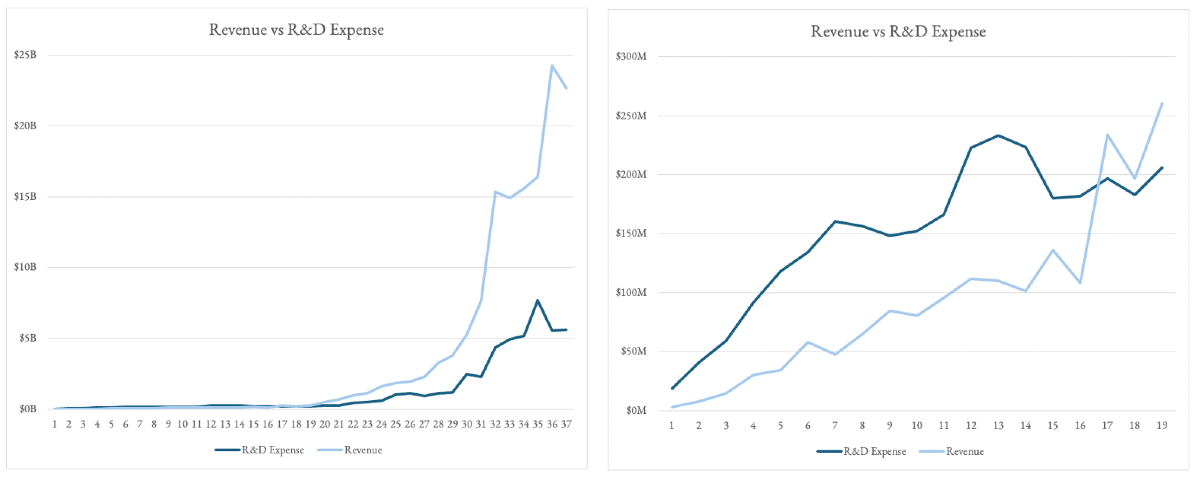

- Revenue plateaus from years ~5-15. The very few companies that make it passed that 10 year lull in sales become the Amgen’s of the world.

- It takes 17 years after IPO for these most successful platforms to have revenues cover R&D alone... and then revenue goes vertical

- Access the raw data here

Building a Biotech Platform Today Guided by Data, Recent Experience, and History

We merge this quantitative framing with our firm’s experience partnering with various platform types and our reading of the biographies of historical platforms to form our views on how to best build a biotech platform today.

Over the last 10+ years, the dominant meta in biotech has swung violently and irrationally between being all-in on maximally general platforms and conservative single assets plays.

We at Compound push back on the recently popularized platform playbook of:

- Raising hundreds of millions

- Then taking 5+ years to build out the most generalized tech infrastructure possible

- Only after that start thinking about what target/disease to apply it to

- And then pursue a pipeline of 10+ drug candidates under the flawed logic of maintaining maximal optionality (which just means that no candidate will receive adequate focus)

The reality is that no matter what, ultimately all platforms:

- Will be judged by their first asset progressed to clinic

- Have little pricing power until proven by stand-out clinical read-outs

- Have at best slightly better odds (i.e. still very low) of developing a successful drug, so building a large, unfocused portfolio is a negative expected value strategy

Moreover, nearly 50% of biotechs go bankrupt due to lack of continued funding vs just 33% for clinical failure. This further accentuates the misguided rationale for maximally general, long duration infra buildout without targeted end-points in mind.

At Compound we focus our bio investing efforts on how to build platforms thoughtfully. We believe that platforms should be built in a step-wise, capital constrained / gated way with a focus on building the initial technology towards a specific target/disease uniquely unlocked by your technology.

Teams should from the beginning have informed views on the range of targets / diseases that they would be uniquely positioned to address.

Not only will this inform the initial tech buildout, but also it will enable you to be in a greater position of strength when you go to negotiate with pharma. Instead of accepting pharma’s list of targets (which will be those that’ve proven impossible for them to drug internally), you can give them a list of target types or targets you’re exploring and partner with them on ones similar to those of interest to you. This may also better align your early partnerships with your vision for your long-term tech buildout, rather than being a speculative distraction.

Then, build the minimal viable tech infra/platform to develop the maximally effective drug candidate for that target(s)/disease(s). The first target/disease is usually not as obvious as Genentech making human insulin, so it’s welcomed to iterate on a handful of targets/diseases before narrowing down and focusing efforts on 1-2 that have an exceptionally strong biological rationale for approval and commercial success.

As those progress towards the clinic, a more full-fledged platform infra build out commences.

Non-dilutive capital from early pharma partnerships funds further investments into the platform… making odds of drug development success tick up and/or making it useful to more researchers and targets… drawing more non-dilutive opportunities… meanwhile, partnering with pharma gives the team a first-hand look at drug development which strengthens the case for internal pipeline development to capture the value you create.

Not coincidentally, the rough playbook above is how the greatest biotech platforms in history were built.

For instance, Millennium got acquired for $9B off of only $8M in VC funding (despite building out custom wet lab automation equipment, assays, etc. which required $50M in annual CAPEX by its third year).

To execute this playbook, it’s essential to have a strong idea of which potential pharma partners have a strategic imperative to succeed in your focus areas, because those are the only entities with whom you’ll have the pricing power to earn a nice premium for all your efforts.

Illustrative mapping from 2020, see here for updated versions

Deal Structure Heuristics

- Sales cycle on partnerships: 6-18 months of hand-to-hand combat with pharma

- Typical partnership value:

- For early stage startups without meaningful platform validation, deals are typically $20-500K

- For those closer to clinic with animal efficacy data deals are on avg: $5–10M upfront + $200–250M biobucks

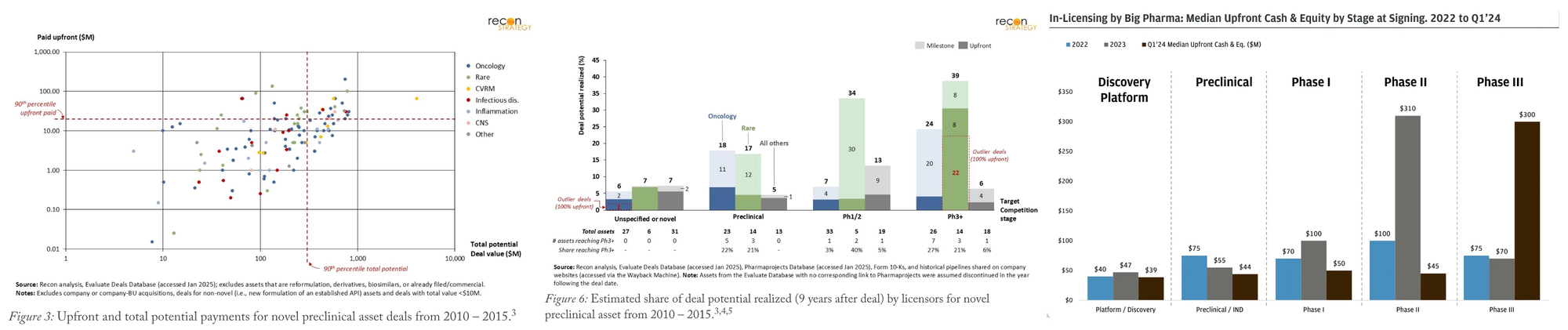

90th percentile from 2010-2015: $20–30M upfront + $700–800M

- Preclinical licensors typically capture <20% of the total deal value after nine years. And payouts are heavily power lawed with the majority of dollars going to milestones for Phase III readouts, blockbuster status, or top 10 deals. Deals on novel or unspecified targets delivered only 5–7% of potential, while those for targets already being pursued by others in trials secured 20–40%.

While the above guidelines apply to all platforms, the nuance of building a platform based around a discovery engine vs a novel modality can be quite different.

Discovery Platforms

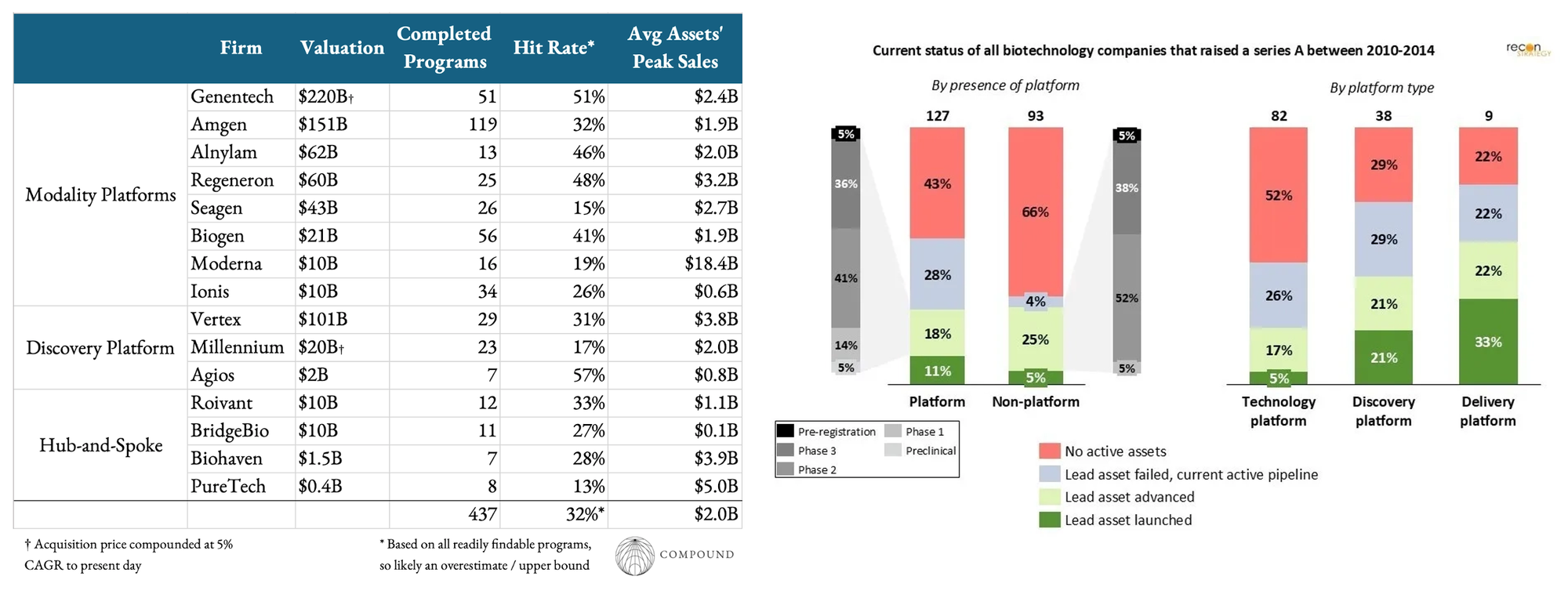

Discovery-focused platforms have historically been harder to build large businesses around than modality-focused ones. As seen in the table above, the only truly stand out discovery platforms in history are the pioneers of rational drug design and of utilizing genetic evidence.

Both turned out to be the rare paradigm shift in the process and efficacy of drug development. Nowadays, developing drugs without any semblance of rational design feels prehistoric. Meanwhile, genetic evidence for drug targets has proven 2x the odds of clinical success, with clear causal genes (Mendelian traits and GWAS associations linked to coding variants) being even higher! We at Compound are excited about parasite-based biomining for the same reason.

To frame the rarity of truly paradigm-shifting discovery processes, consider that the number of novel targets approved by the FDA each year is usually between two and four.

The reason for this historically greater difficulty might lie in the difficulty, long duration, and capital intensity of getting a novel discovery process to a minimally disruptive product and product-disease fit. As such discovery platforms start off as point solutions, it takes heightened clarity to get to a disruptive process within a couple years.

Put more bluntly, it’s historically been easier to commercialize a novel modality capable of expanding the targetable space than to reinvent the scientific process itself.

Modality platform biotechs sell end products to pharma, not data/information/insights. The latter is far harder to patent (i.e. one can’t patent targeting a biological pathway). And, the history of data in the biopharmaceutical industry is the history of its commoditization. Companies that live and die by their drug products are naturally motivated to make data pre-competitive, at least once they've extracted their proprietary edge. They do not want to be held hostage by the owner of information.

Because pharma has been reluctant to pay more than minuscule amounts for pre-clinical information or change their workflow around novel technology, discovery-focused platforms tend to adopt a JV-like business strategy of orchestrating their own tech to help pharma hit difficult targets. It also means that discovery platforms tend to need to move faster up the value chain into an integrated internal pipeline than modality companies.

This industry dynamic of pharma paying pennies for pre-clinic discovery tools may change if and only if pharma starts to view novel approaches as existential threats. We're currently seeing this within our portfolio across multiple companies as incumbents/OEMs show increasing urgency to work with companies like Wayve, Runway, Orbital, and others.

We at Compound expect these problems will be increasingly alleviated under the theses that:

- It may be quicker to build computational tooling that’s useful than whole wet lab flows

- There’s now enough tools at the industry’s disposal that a newcomer building a step-function better point solution can slot right in before expanding its offerings over time

- Pharma will internalize in the next five years that these information-based platforms are serious threats

- ML discovery engines that benefit from ever-more data can have an improved tradeoff to partnerships. Historically, they’re viewed as selling future value for cash in the present. But in theory, platforms that compound with data can enjoy both the cash / legitimization in the present and the increased likelihood of future programs.

The start to this year gave a hint that maybe this shift is happening within big pharma. Noetik, Chai and Boltz all secured 8-figure model license deals with some even being non-exclusive. Time will tell if this is a fad or if the ROI pans out.

Either way, we are exhilarated by the dozens of emerging technologies to bend the probabilities of discovery and have been investing in many different versions.

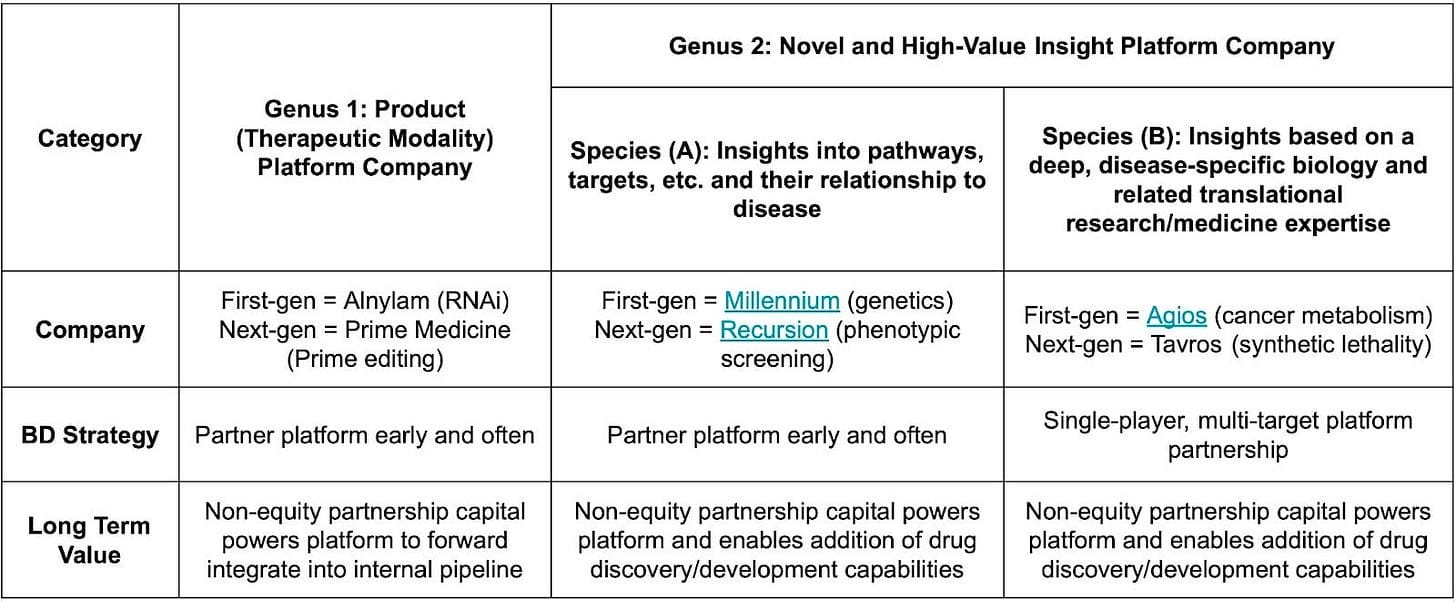

Broad vs Deep Discovery Platforms

Insight platforms come in two broad forms. Some have broad applicability across many biological pathways and drug targets like Millennium with genomics. Others take a deep, disease-specific approach. Agios is one of the most successful cases, built around metabolic insights into cancer.

The narrower the platform's focus, the more it starts to resemble a product company. Fewer shots on goal means each one must count. In practice, that means landing a large, multi-target foundational partnership early and then pushing hard to advance internal programs alongside it.

Modality Platforms

As modality platform biotechs sell end products to pharma, they've historically fared best. Millennium CBO and biotech vet Steven Holtzman put it best:

“In general, if you are a Product (Therapeutic Modality) Platform Company, your primary risk is under-spending/under-capitalizing early:

– Your value is directly driven by your first-mover advantage.

– You need to drive as many shots on goal as possible.

– You need to stay ahead of the pack in the perfection of your platform/product engine: be, continue to be, and be perceived as the leader.

Because you have a potential “embarrassment of riches,” you can partner early and often to raise non-equity capital because whatever product rights (= source of long-term value) you monetize, there will be more where those came from.

Early deals can give away all product rights, e.g., to a disease area, maintaining only a downstream economic interest (typically, milestones and royalties).

In the next step, the ability to “belly to the bar” for greater downstream financial participation (cost and profit share) will likely feature without commercialization rights.

In the following step, some level of commercialization rights (co-promotion/ geographic splits) will be added to the cost and profit share.

In a possible next chapter, the deals may add on full commercialization rights to one or more of the products coming from the collaboration (e.g., via a picking mechanism).

It is the author’s belief that you are better off sharing in all of the fruits of the collaboration with profit share and retention of a geography and/or co-promotion than in going with a picking mechanism to provide forward integration to commercialization ability. Picking is a binary bet…spread the risk.

The combination of a high stream of non-equity capital and clarity that you are using that to build out the leading platform while, at the same time, you have retained enough opportunities for forward integration into downstream value, will drive your stock price up. Now is the time to use the equity markets as your primary source of capital to fuel your retained product opportunities.”

Historical Base Rates for New Modalities

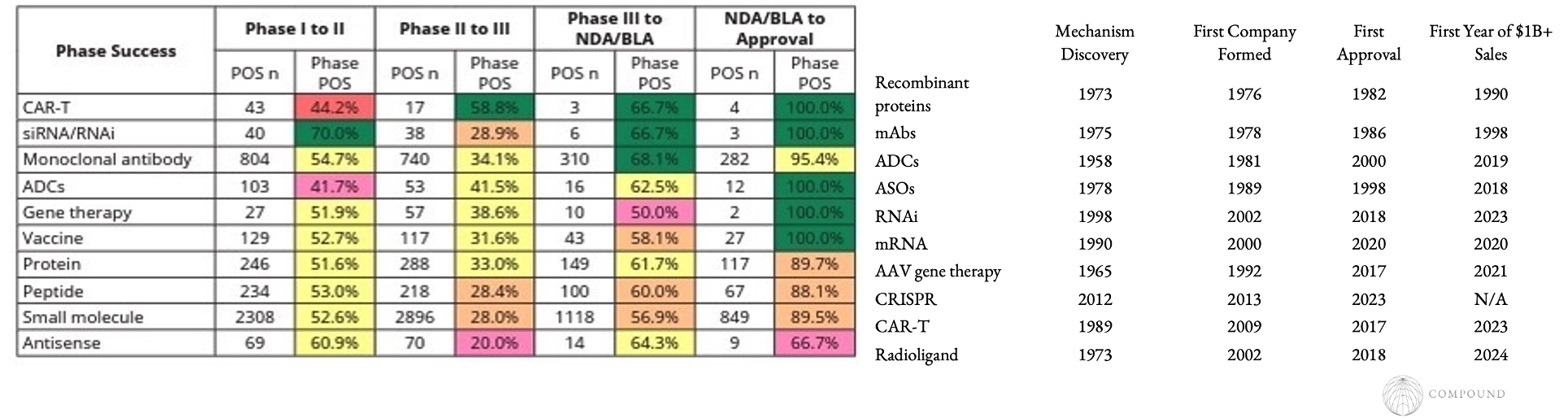

A review (albeit with small n) found that new modalities can have higher success rates than small molecules.

First companies to translate a novel therapeutic modality from academic labs to human trials (e.g. Genentech, SeaGen, Alnylam, Ionis)

- Fairly often emerge from the lab that made the initial discovery or at least made a major leap towards therapeutic relevance

- They take several decades to build, because almost all modalities go through hype cycles. On average, it takes 30+ years to go from discovery to a breakthrough drug.

- ~13 years to go from discovery to first company formed

- ~14 years to go from first company formed to first drug approved

- ~7 years from first approval to the first year a drug does $1B+ in annual sales

- We at Compound expect that historical timeline to shrink meaningfully over time. Still, during that multi-decade slog, even the companies that now define their modalities regularly experienced existential doubt. It takes a certain kind of leader and culture to persevere.

- Era-defining companies are often companies that are first to pioneer a new modality, reaching $10-100B+ valuations.

Companies innovating on established therapeutic or delivery vehicle modalities (e.g. Dyno, BigHat, Fate, Abcellera, Adimab, LabGenius)

- These companies commercialize a step function improvement and / or a process innovation that enables them to continue to optimizing existing modalities over time

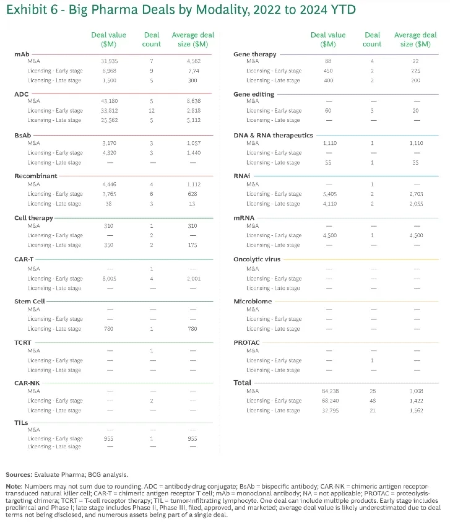

- They generally don’t require multi-decade journeys and if they solve a crucial bottleneck in a hot area can even be $2B+ takeout targets within a couple years of founding (e.g. Aliada)

- Hot later stage companies can often get $30-150M upfront with $0.5-1.5B+ in biobucks per partnership

The Constant in a Cyclical Industry

The hot technology of the moment rises and recedes, passing in waves. What the market deems uniquely valuable shifts. The goalposts for what gets an A done move.

Yet the core strategies for building enduring platforms have held stable. They've worked from the birth of the biotech industry to today, and we expect them to keep working until the data proves otherwise.

Biotech platforms are one of our most core focuses at Compound. From new modalities (e.g. Polyphron doing tissue replacement, Juvena doing secreted proteins, a mini binder company) to tech platforms (e.g. Achira doing NNPs) to insight engines (e.g. Pheiron doing population scale biobanks). We publish our theses for new startups here.

If you’re building a novel platform of any variety, we’d love to chat.