Playbook for Diagnostic Companies

A core belief at Compound is that net new data collection can both solve urgent clinical bottlenecks and will become increasingly valuable in the AI era. We’ve met many founders aiming to translate their novel diagnostics assay, with varying degrees of sophistication on how to actually commercialize it. We hope this playbook helps you think through how to quickly and cheaply launch and to navigate building a durable business model.

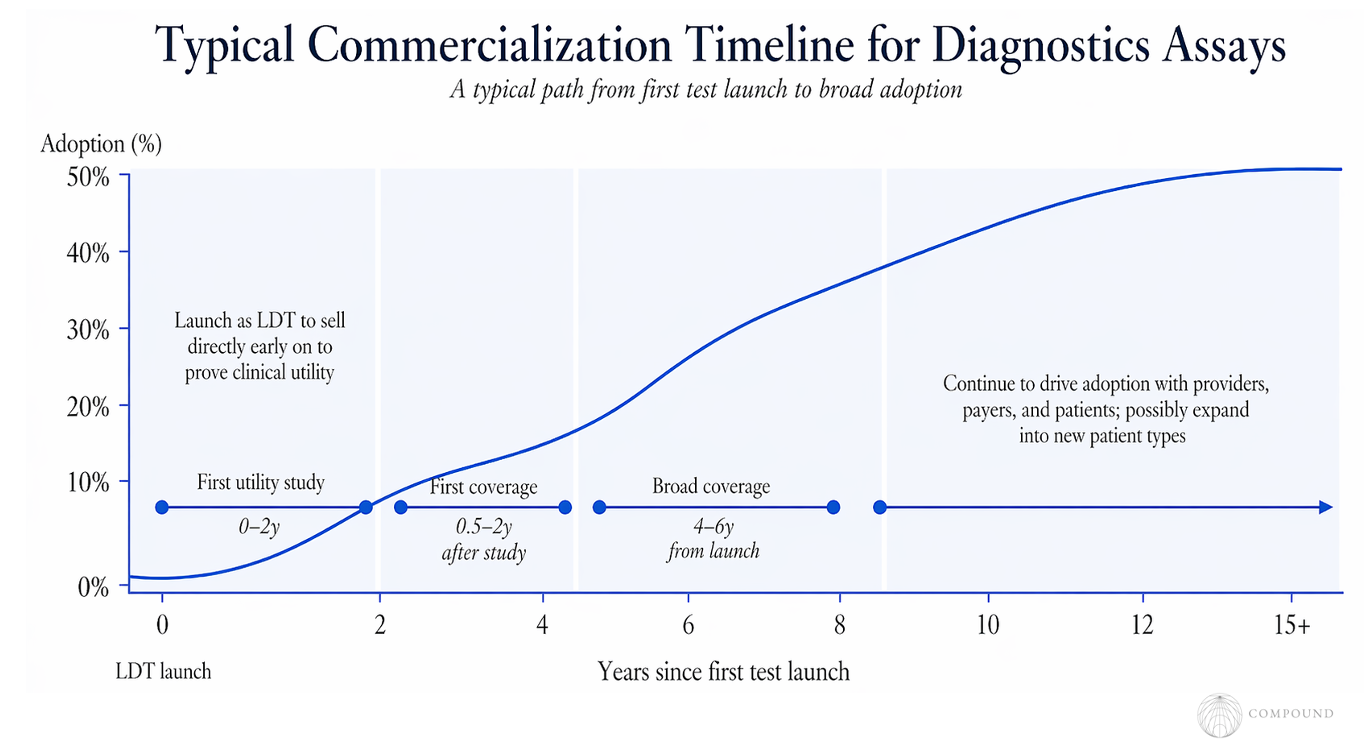

Launching Quickly & Proving Utility

It’s generally best to launch with the LDT pathway, which doesn’t require FDA approval or anything other than spot checks of documentation during routine lab inspection. Companies can sell directly to patients before getting insurance and Medicare coverage. In fact, some public companies reached high 7-figures in patient-paid revenue, with a couple examples pushing into 8-figures and Grail at $150M without reimbursement.

That real-world usage helps build up the case for clinical utility, which can be furthered in the meantime with CPV vignettes.

Companies typically publish their first study that points to utility in the first 0-2 years after launch. The timeframe for companies to run their first clinical trial varies far more widely, with some doing it before launch and some long after. For what it’s worth, the median is ~6 years after launch.

Reimbursement

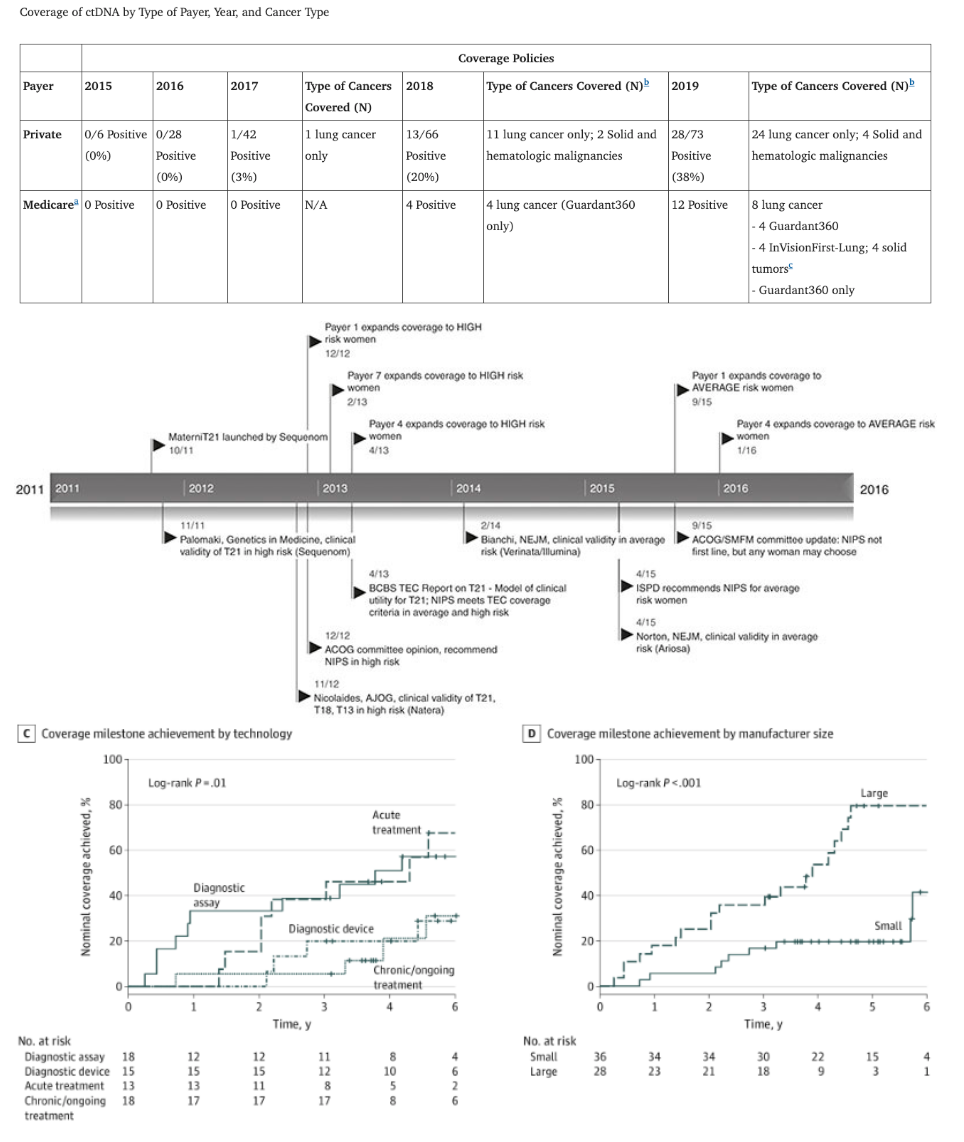

From the first study clearly indicating clinical utility, it typically takes 0.5-2 years for the test to get its first coverage, whether that be a payer and/or local or national Medicare coverage. Coverage often then trickles through other payers until it has relatively broad coverage 4-6 years after launch.

This dynamic can be seen at both the levels of individual company tests and at the entire categories of tests like ctDNA cancer diagnostics vs prenatal screening.

Payers evaluating whether to reimburse a test focus dominantly on utility: does the test change the course of clinical treatments and health outcomes for the better, with price being a distant secondary concern.

Further follow-up utility studies can get the coverage to expand for instance from high-risk individuals to average risk or from lower fidelity less expensive tests to higher fidelity ones.

Another route is through reinsurance, as Grail got Munich Re on board even without reimbursement. Though, as of 2024 they'd only contributed to 7k tests.

For more tactical details on reimbursement and coding, see this review.

Full Commercial Rollout

The full-scale commercial rollout then typically unfolds over 10+ years. Beyond proving utility, eventual sales can be boosted by purposeful engagement with KOLs like those viewed as clinical leaders, those with high volumes, and medical societies early.

Once a clinician adopts using a test, it can be fairly sticky. NRR amongst physicians that have already ordered tests can be 85% and even as high as 115%.

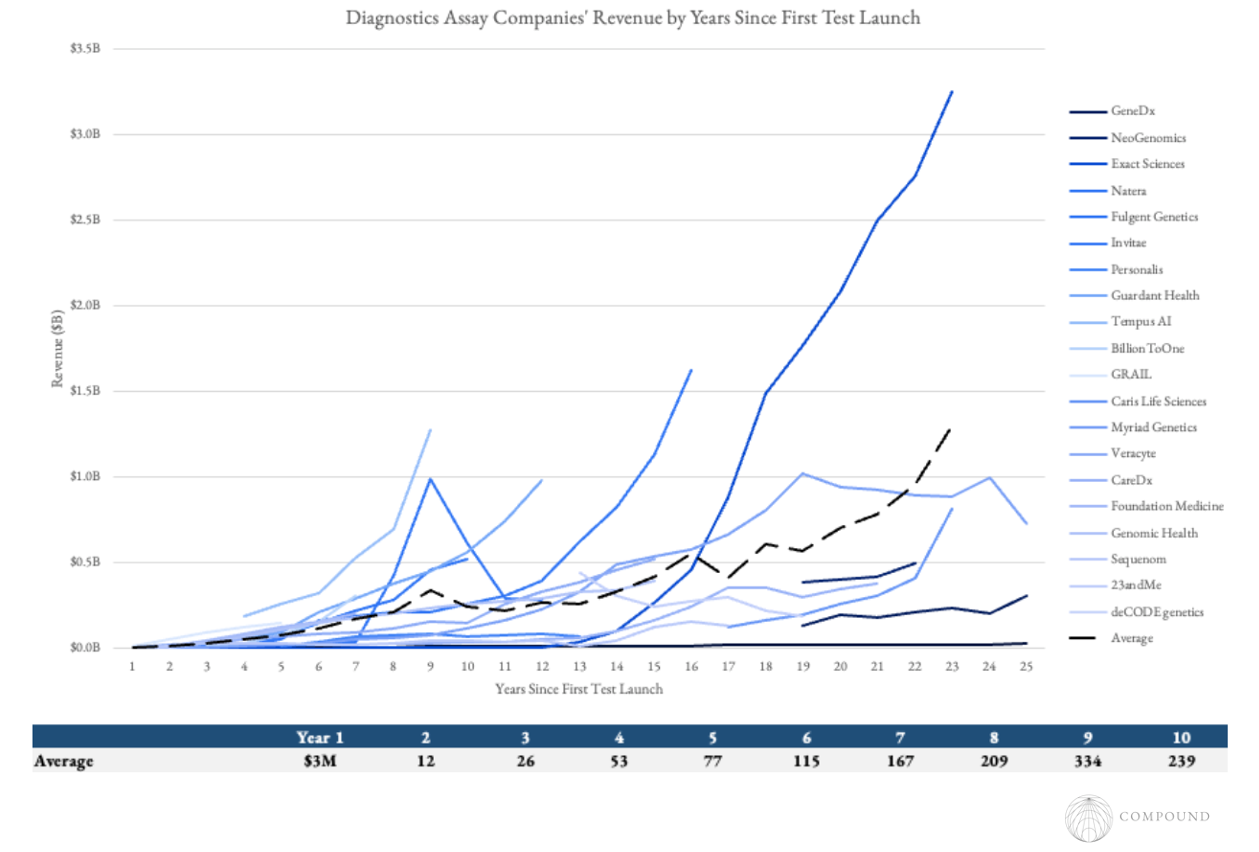

While most successful diagnostics today are decades in the making, some examples like BillionToOne scaled PMF more rapidly, hitting $1B in sales 8 years after launch. The largest driver of their success appears to be that their test was for years the only one that entirely removed a crucial friction point in the clinical process, rather than incrementally higher accuracy data. In their case that was the need to schedule a second test with the father after a positive maternal prenatal test and fathers showed up <60% of the time.

Beware that even after a test type has been rolled out successfully, claims denials can still be a meaningful problem. The oncology NGS claims denials rate for Medicare enrollees from 2016 to 2021 was 23% and increased over time. In general, claims tend to be lower for hospital sites, for less expensive or essential tests (e.g. <50 gene panels), in-network payers, and for those that have set up up-front workflows like prior authorizations.

Diagnostics Companies’ Financial Profiles

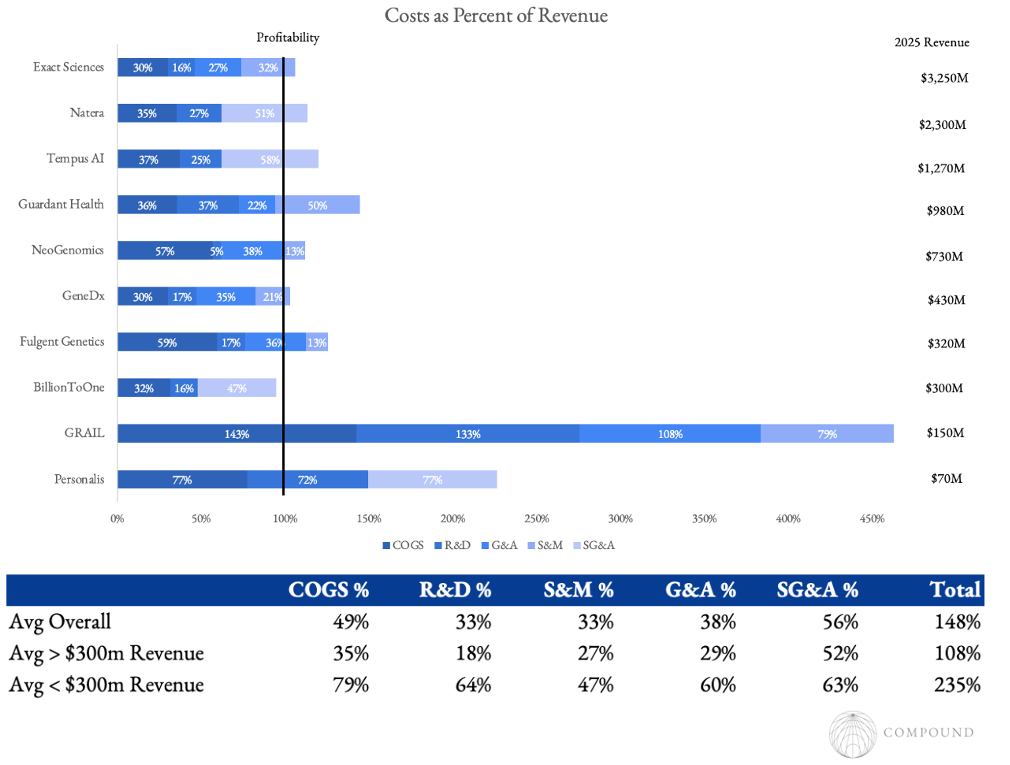

In general these businesses have struggled to reach breakeven. To our count, just 4 of 20 public independent diagnostics assay companies (i.e. not Roche, Labcorp, etc.) have reached profitability including those that have been in operation for several decades.

Importantly, these businesses usually have significant operating leverage. For companies below $300M in revenue, each major expense category as a percent of revenue is 2x that of companies above that threshold.

A core driver of that is it takes tremendous spend on trials to build out the clinical evidence base and on clinician education for the clinical network. And at first the lab itself hasn't gained factory-like efficiency and has near-zero volume to amortize the overhead. But as that solidifies and more payers actually pay for the test, the economics can quickly flip. The company no longer spends much on trials, convincing clinicians, or payers.

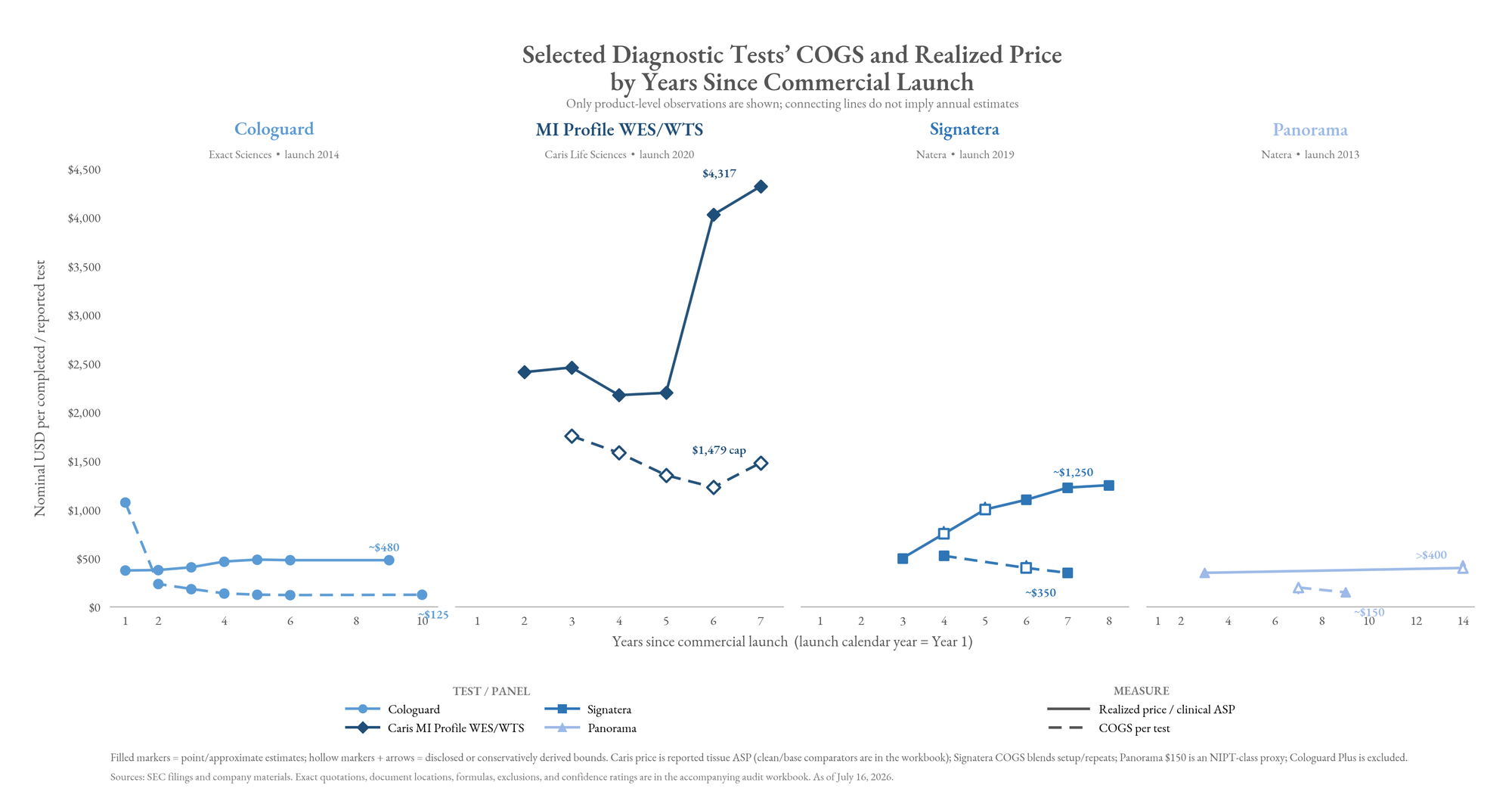

It's common for realized ASP to double and COGS to halve over the years since commercial launch, causing profitability per test to 4x. For instance, Medicare’s Signatera ADLT rate increased from its initial $3,500 to $3,920 in 2022, but realized ASP remained much lower because many tests were unpaid or paid by lower-rate payers. As more indications obtained coverage and the probability of payment increased, blended ASP moved toward the paid-claim amount.

And, clinicians start ordering higher volumes of tests since the tests are sticky with 80-120% NRR. For instance, Guardant saw average demand per physician more than double from 12 tests in 2021 to 26 in 2025.

Revenue = p * q, and both can increase by multiples, enabling the steady compounding towards profitability.

One interesting dynamic for new startups is that they slot into existing codes and price points. So if one can drastically decrease the cost of the assay, then that flows directly to the bottom line. For instance, EarlyDx reduced the ctDNA cost to $20 by enriching for the methylated segments before sequencing but still charges the standard $1,000. Meanwhile, Goodfire and Prima pioneered a different path by employing mechanistic interpretability on a genomics model to isolate the signal that the model keyed in on to make its predictions, which turned out to be a far simpler biomarker and could yield a cheaper diagnostic.

Also, companies with large test volumes could get leverage by applying AI to discover and produce far cheaper reagent proteins (e.g. see our thesis here). Reagents are ~40% of COGS and ~12% of total expenses for scaled companies.

(Relatively) Newly Scaled Business Models: Data and Partnerships

While companies like 23andMe and deCODE pioneered early versions of combining diagnostics with data sales and/or drug discovery partnerships, their companies’ were organized around either diagnostics or those alternative business models and only tried to meld both together after their core business started to struggle.

Whereas, Tempus built their company from the start around industrializing this hybrid business model.

They spent ten years building out not just their 450PB of data, but also their tech stack. All molecular data is contextualized and connected to longitudinal outcomes; they have real-time outcome/response tracking; enterprise Lens access, productized cloud/compute, and analytics on top. Then, that package is sold by 30 BD executives focused solely on data.

They have demonstrated how lovely the synergies can be. Their per-patient diagnostic generates $1,200 in revenue. But they explicitly view this as data-acquisition. As of 2018, Tempus made 7.4x more revenue per patient on data licensing, analytical services, and clinical-trial matching than the sequencing alone. That revenue stretched over the subsequent six years, with $16M, $13M, $7M, $6M, $7M, and $7M respectively. And that second-order revenue runs at 65-80% gross margins with 125-140% NRR.

They turned a one-time service into a recurring revenue annuity with software margins.

But this business model requires the organization to be organized around it. For instance, even though Caris has almost as large of molecular datasets as Tempus, its data licensing business is struggling to take off. It launched in late 2022, but they haven’t re-oriented the company's DNA around it and the CEO recently said: “We’ve always been clinically focused. We’re always going to be clinically focused.”

Current Competitive Landscape

Where to Next?

Towards ever easier and more passive monitoring

A core thesis at Compound is embedding health monitoring ever-more non-invasively and passively into the backgrounds of our lives. For instance, we published research and hosted a conference a year ago about biochemical wearables, smart toilets, and implantables. We published our mapping of the year-by-year future of biohacking. And, we’ve invested in several companies on this thesis like Atlas and Alljoined.

We envision futures that include:

- Early detection tests for major diseases like multiple cancers, Alzheimer's, etc. being lumped in with regular blood tests like those of Function

- Molecular testing toilets like that of BiomeSense improving colorectal cancer screening from colonoscopy to now Exact’s stool test to 24/7 in the background

- Wearables and sleep data fully passively providing sparse signal of disease phenotype before symptoms

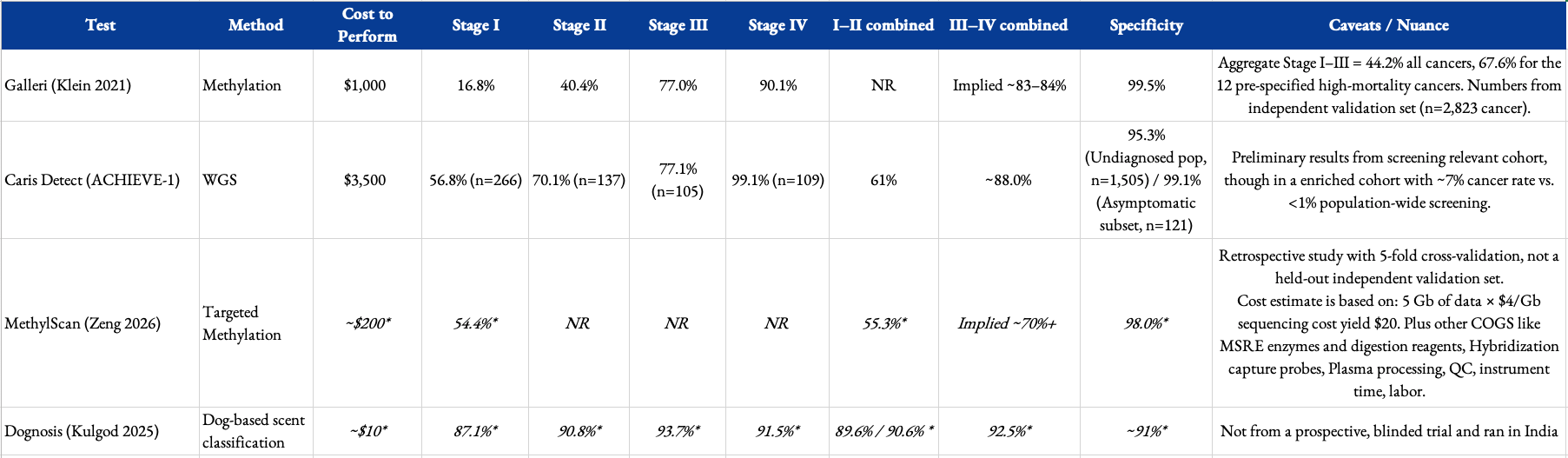

- A scent sensor with dog-like sensitivity embedded into your pillow for passive detection of disease signatures in breath (e.g. Dognosis just reported 91% sensitivity for stage I & II cancers in their clinical trial for breath detection)

Achieving these futures will require additional breakthroughs that we’d love to support. For instance, current multi-cancer screening tests like Grail’s have shown promise and demonstrate the market but have repeatedly failed in large-scale clinical trials to show clear benefit due to limited specificity. It had more false negatives than true positives and still has low sensitivity for early stage cancers, reporting 17%-37% for Stage I and 40%-70% for Stage II. Moreover, the fact that it only detected 3 cases per 1,000 assessed people in a 142K person trial of healthy 50+ year olds underlines the difficulty of untargeted continuous preventative screening especially with current technology. This can undoubtedly be improved by screening based on risk factors. We’re excited about approaches that could yield far higher performing MCED tests by for instance combining more modalities when complementary and using methods like mechanistic interpretability to isolate the sources of strongest signal.

Cheaper and/or more comprehensive testing

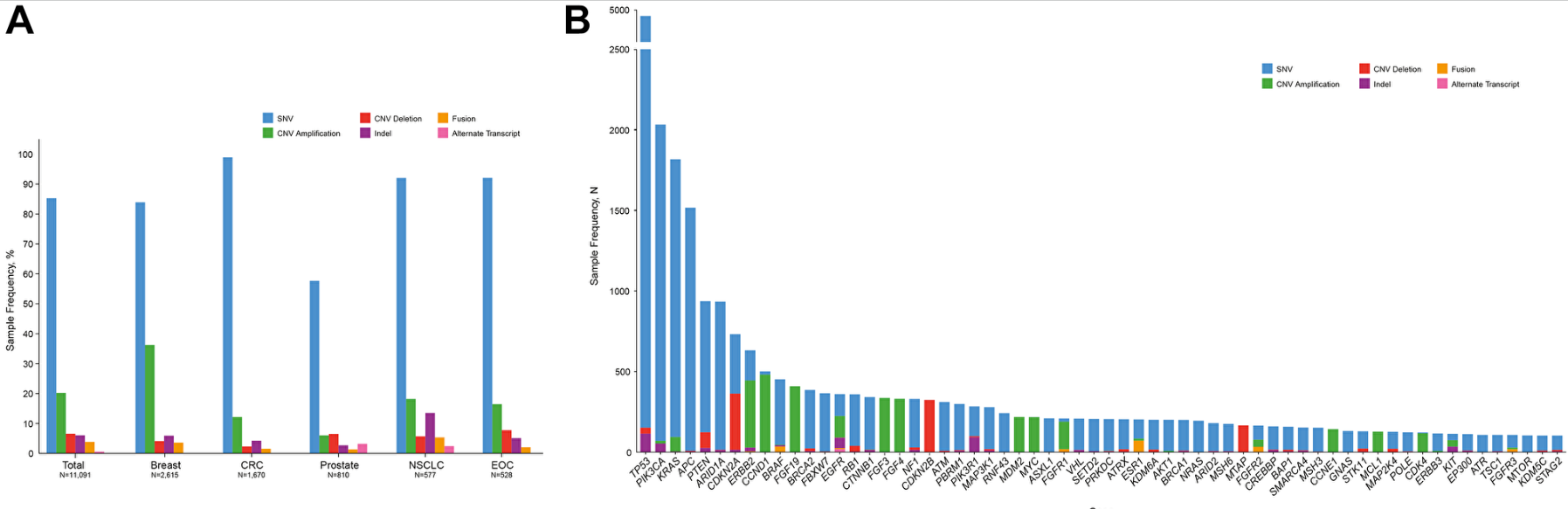

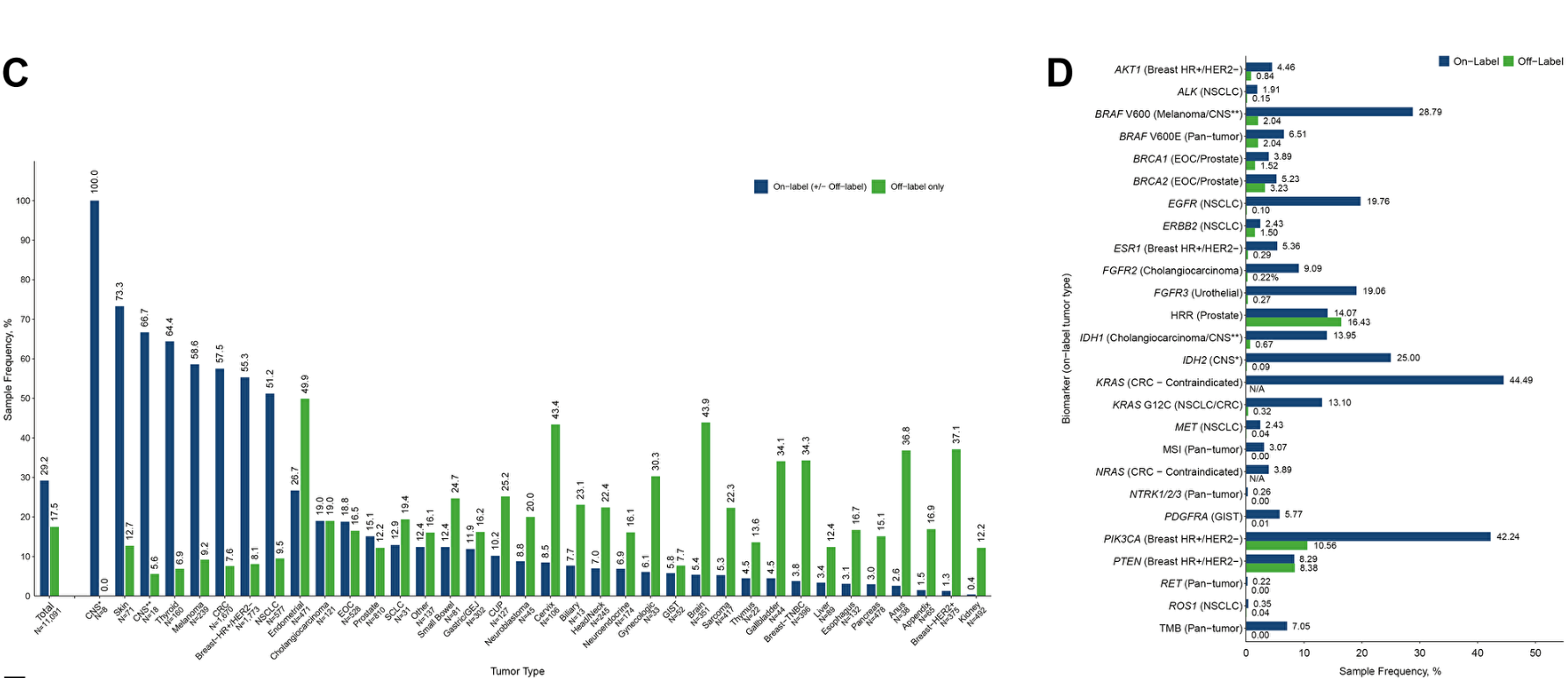

Startups whose core pitch is more data points must be extremely careful that their incremental data drives different treatment decisions and is essential to improving outcomes. The ctDNA cancer diagnostics sector is currently wrestling with this. Because cancer-driving variants follow heavy power laws, a simple <300 gene panel covers 85%+ of druggable targets. The newer WES + WTS tests determine decisions in generally only the long-tail of patients. For instance, transcriptomics integration informs as much as 40% of actionable findings in patients with rare or unknown cancer types.

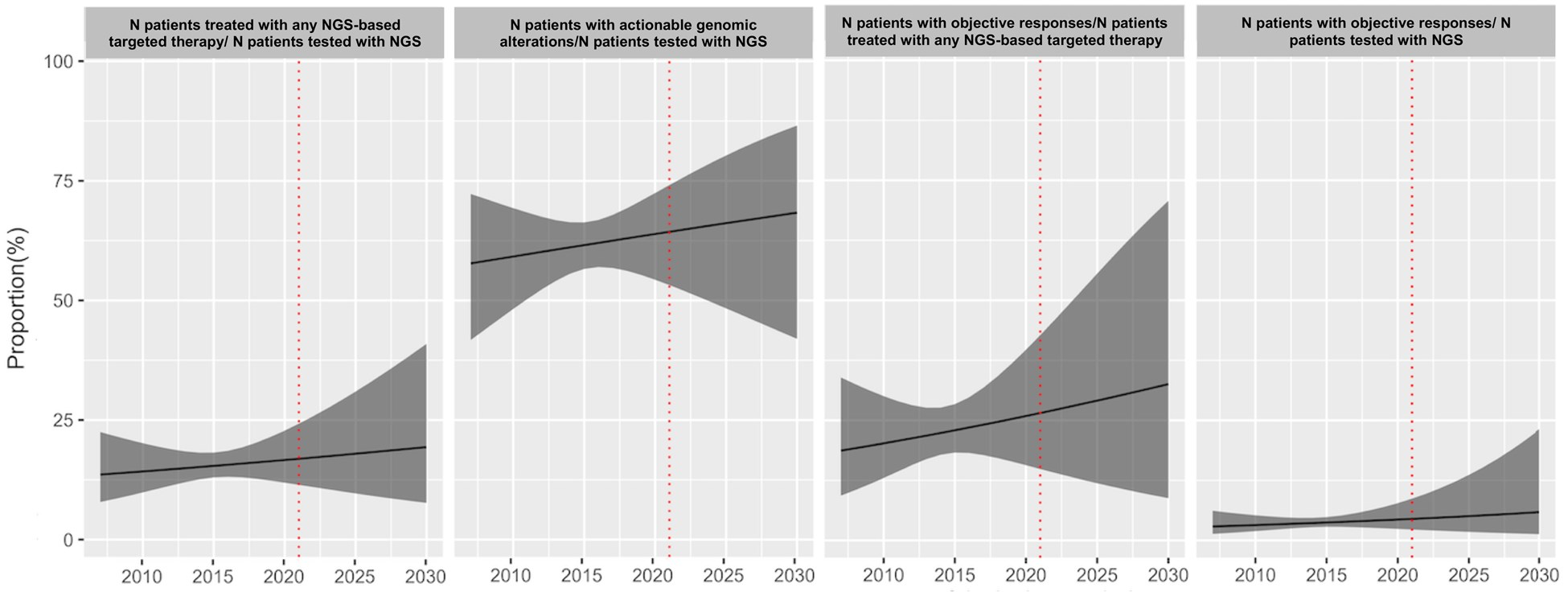

To give a sense for base rates here, comprehensive gene panels in solid tumors find actionable variants in 60% of patients, but only 15% of patients receive treatments based on the test results. Patients that do receive test-guided treatments have better outcomes but somewhat marginally so with a boost in ~2 months of PFS. Prospective and even retrospective trials have struggled to show clear clinical benefit of these more comprehensive tests for broad populations. It tends to be more effective for certain subgroups like rare diseases.

However, these markets are still early with ~60% of patients still not getting even basic gene panels and <5% get WES + WTS. The therapy selection market broadly is only ~35% penetrated.

These tests will get ever-more useful over time as increasingly targeted therapeutics reach the market. This is true even for WES + WTS, especially for personalized neoantigen vaccines or therapies, expression-based T-cell/ADC selection, and genome-wide HRD/signature use.

All of this is to say that for cancer or any other area, new tests boasting ‘more data’ must have a clear rationale for how they’ll improve outcomes and/or be the same cost as simpler tests such that there’s no tradeoff.

We’re excited about those inventing fundamentally cheaper proteomics assays for a next-gen Function Health, far cheaper WES + WTS assays such that they become first-line default, even more comprehensive testing for rare or hard-to-treat cancers, breakthroughs for cheaper MRIs for continual health monitoring.

Diagnostics companies owning the customer interaction and moving up the stack to embedded intelligence

Diagnostic tests can be thought of as the edge intelligence needed to make a decision, in a time when intelligence is getting cheaper by the day. The industry is converging towards vertical integration from many different starting points each with their own corresponding flavor.

- DTC product companies: companies like Function Health, Oura, and Hims are trying to crosssell anything that they can beyond their initial product to build a fuller service platform to aggregate demand. They’re now starting to provide advice themselves and route to doctors. Who knows, maybe their paths will cross with digital doctors companies like Doctronic coming from the opposite direction.

- Traditional scaled diagnostics & pharma going DTC: half of all new Zepbound prescriptions are filled through Lilly Direct, Novo Nordisk partnered with Hims & Hers to distribute through its channels, Caris partnered with everywell to sell cash pay to consumers, etc.

- Care providers: companies like Compound portfolio company Valius that spun out of Sid Sijbrandij's universe to productize the “maximalist approach to cancer” he pioneered for hard-to-treat cancers while providing the in-person care themselves

The arch bends toward more data, more insights, lower cost, easier customer experience. But the devils in the details. We’d love to discuss them with you!

See here for our full dataset