Transcending Water’s Zero-Sum Trap

Similar to how electricity costs are becoming a core political issue at the same time that technological solutions have reached maturity, the gradually widening supply-demand mismatch for water lays the foundation for such a moment. When trying to identify a catalyst for what makes these things crack, the emerging belief that data centers guzzle water may be the trigger.

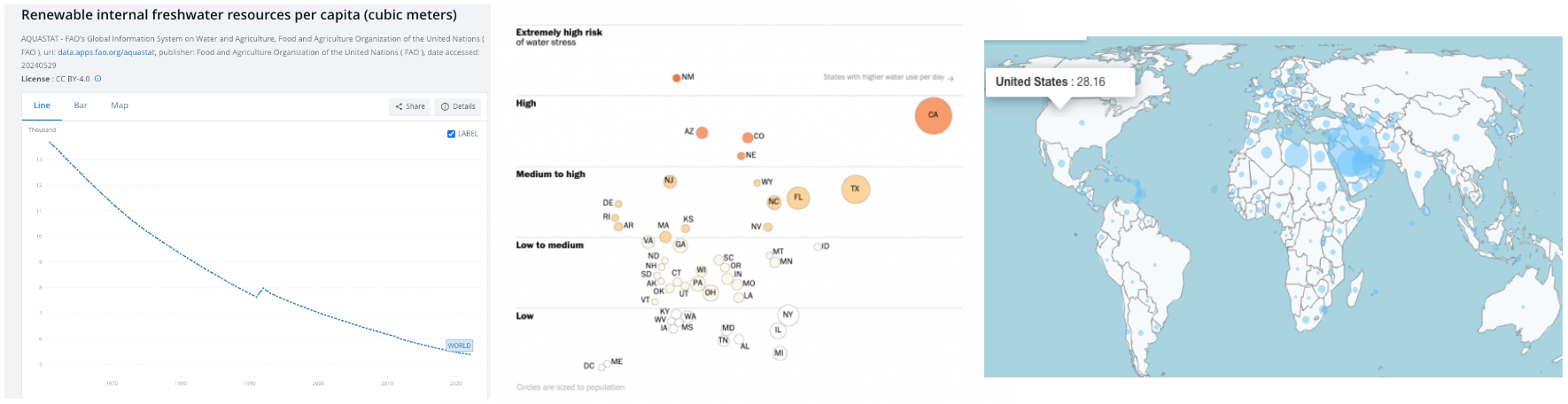

Water resources have slowly been drained, with primary water supplies already at concerning lows. The two lakes that supply much of the southwest are 28% full, near the minimum threshold to generate hydropower. Likewise for the San Antonio valley. Global warming is expected to further reduce supply by 10%+ over the coming decades.

The political pain has started. States along the Colorado River agreed after years of infighting to a rationing deal where they collectively cut their demand (largely cutting farm output) by 13% in exchange for $1.2B from the federal government. Arizona had to decide between allowing TSMC to build a cutting edge semi fab or allowing population growth in certain cities. Meanwhile, the eighth largest city in Texas is in an existential crisis after running out of water thanks to an exhibition of some of the worst governance you’ll ever come across, as detailed in this NPR essay that reads like the Onion.

For residents, he said, life might be like it used to be for him, 70 years ago, as a boy in the Rio Grande Valley, when he would hang plastic jugs on mesquite branches and carry them on his shoulder to ask nearby companies for water. “This is the legacy of the imbeciles,” he said.

Politicians try to blunt the effects from consciously reaching their constituents by artificially suppressing prices below market rate with subsidies and rationed demand. Water’s often even priced well below cost-recovery levels, with some nations like Italy pricing 55% below cost recovery!

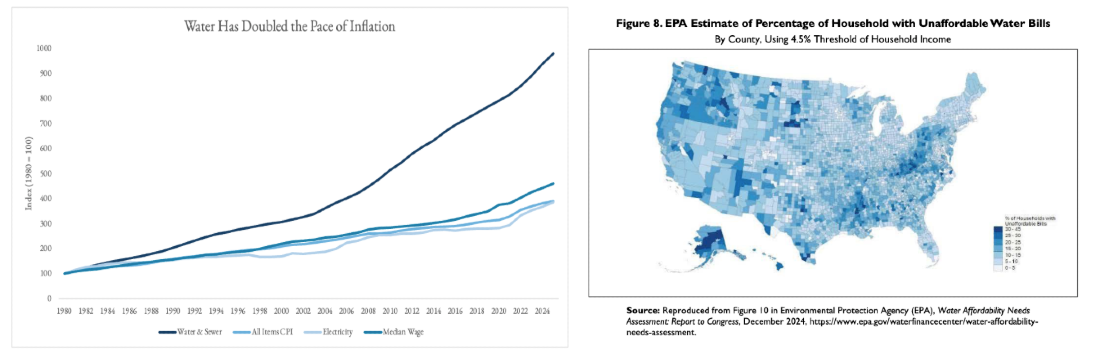

Despite that, water has sneakily been one of the few things doubling the rate of inflation and wage growth. This has made it increasingly unaffordable in many counties across the U.S., with water bills reaching 4.5% of household income in some counties. With global warming further crunching future supplies, water’s salience will only rise.

Desalination & Wastewater Treatment

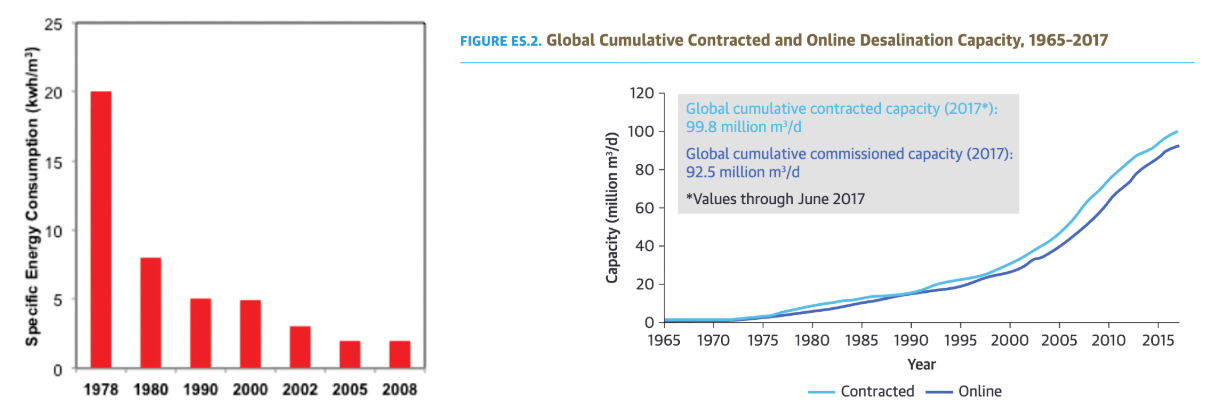

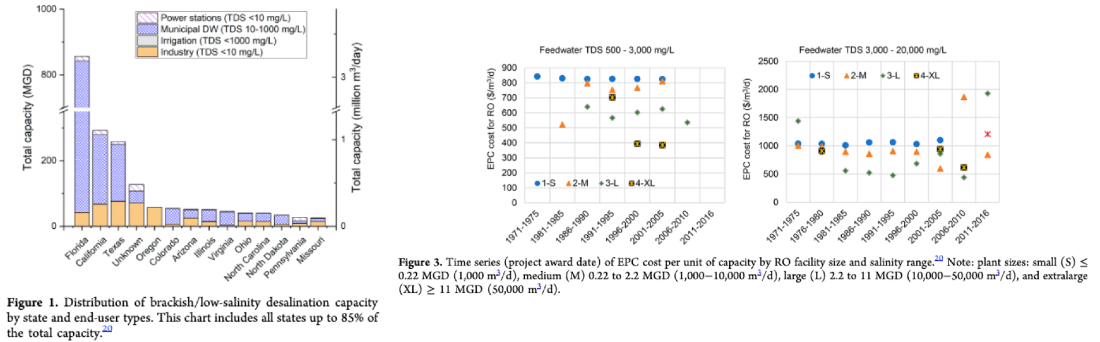

After falling 10x in cost over the decades, the technological solution to scarcity has matured to the point that it’s now within range of freshwater costs. Brackish water is now 1.5-3x freshwater’s cost and seawater desalination is 4-6x. Over 20,000 plants now operate throughout the world. The global desalination market has grown at a 9% CAGR for decades. In the US, more than 40% of commercial and residential water supplies come from desalination and wastewater reuse. 100% of the municipal water supply in the UAE is desalinated.

{kind=link}

Unfortunately, in its current form, its deployment in the West is almost as politically challenging as nuclear before it became cool again. California requires 27 permits to site a desalination project and can take decades. For those brave enough to try, many large projects in even the most water stressed regions like Los Angeles and Corpus Christi get rejected for a combination of environmental concerns over the brine discharge, harm to sea life from sweater intake, and cost.

New Technical Breakthroughs and Business Models Needed

Banging your head against the political machine wall is unlikely to yield dramatic results. Creativity will be required to scale in the US and have a shot at truly solving the scarcity at hand.

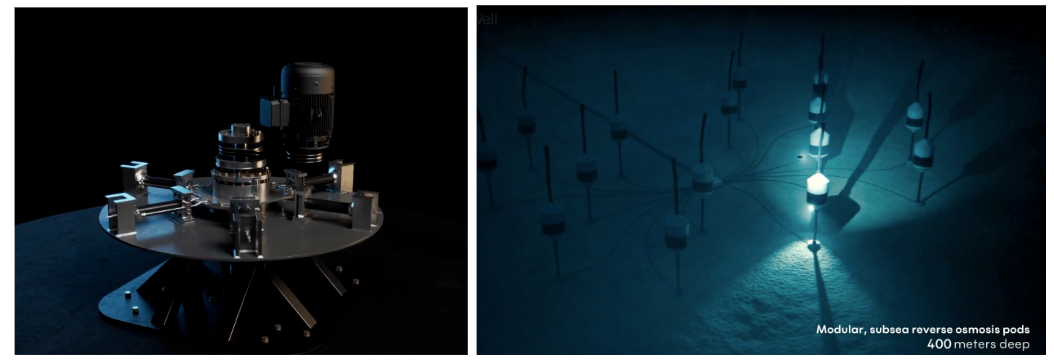

The two main research thrusts are (i) novel membranes or solvents and (ii) efficiently creating pressure. The latter boasts some fun ideas, with some pursuing centrifuges, others putting desalination pods 1,000+ ft below water to benefit from its 30x higher pressure, still others harvesting wave motion.

Even with these creative approaches, we haven’t seen any that on the first of a kind plant aim to beat reverse osmosis on cost, no less bridge the gap to surface water.

We actually don’t see that as an unassailable barrier, though we’d certainly like to see systems that eventually bend the cost curve. For now, the larger differentiators seem to be the squishier need to remove arguments against desalination and separately innovate on the business model and GTM.

The traditional approach to water processing is a poster child for something that’s not venture backable. $1B in capex. Selling to municipal governments (yes it’s often plural), requiring a 3+ year sales cycle even with demo-ready technology. Water utilities control the canals and pipes that any startup must connect to. The average M&A exit multiple is just 2x sales.

Selling equipment to desalination plants or integrated players like Veolia / Suez can be moderately easier. Smaller desalination organizations' total sales cycles are 6-8 months including ~4 months of testing and operate 100s-1,000s membranes with contracts of <$5M. Larger desalination organizations' sales cycles are 12-24 months including ~12 months of testing. One large-scale plant has 30,000+ membranes for a deal worth roughly $40M.

Despite desalination benefiting from economies of scale and the municipal market being larger in TAM, the most (and seemingly only) viable GTMs we’ve seen involve smaller scale units sold to industrial partners.

Yep, you guessed it: data centers!

Animosity toward datacenter buildouts grows daily and now 50% of datacenters get rejected. The #1 reason is… water.

The fact that these campuses don’t actually use much water is irrelevant, because the perception is all that matters, and those opposing them likely want to believe they do given anti-Big Tech / -the Man sentiments.

Currently the hyperscalers’ water offsets are largely greenwashing, like marsh restoration grants.

The key will be to normalize a contract structure where hyperscalers contract with the startup to build decentralized desalination that makes their water use at least net zero. And perhaps even provide water back to the community. Google pioneered this structure in electricity markets with PPAs nearly 20 years ago where they pay for the construction of energy (often renewable) either onsite or offsite, whatever makes more sense.

Equally essential is producing no brine discharge (i.e. zero liquid discharge) to leave no rational arguments left.

This market could scale quickly and reach a $10B opportunity by 2030. And again, this would (in principle) solve the single biggest blocker to datacenters for the highest urgency and most cash rich customers in history.

The second viable GTM we’ve come across is advancing a technology capable of processing hypersaline or otherwise challenging wastewater. No approach has successfully solved this problem yet despite appealing initial customer sets including oil & gas, semi’s, and lithium brine mines.

For context, each barrel of oil, 5x that much hypersaline produced water is generated. Currently O&G disposes of it largely by injecting it underground. This suspect disposal method is starting to draw a raised eyebrow from regulators. More importantly, injection disposal costs $0.60+ per barrel with pipeline infrastructure and up to $2.50 when transported via truck. That’s ~$35-$47 per 1,000 gallons or roughly an OOM more than the ~$4 one can get for municipal water.

What makes this a viable path for startups is that these O&G giants require the tech they procure to be able to rapidly scale. A single company’s contract order following the initial demo can quickly reach hundreds of desalination units. Indeed, the only venture-funded water tech company to become a unicorn started in treating O&G wastewater and reached $200M in revenue with $550M in signed contracts.

The Permian Basin alone creates 7.3 billion barrels of produced water a year! That’s a ~$4B revenue opportunity unaddressable with today’s tech.

A company that solves this hypersaline wastewater could then move into minerals extraction like lithium brine for which the unit economics are similar. And then to brine discharge from existing desalination plants. Seawater RO plants only recover 40-55% of the water they intake, with the rest being discharged as hypersaline brine. Pushing that towards say 90% with a zero-liquid discharge technology could fundamentally change the economics of these $1B capex plants, bend the cost curve of desalinated water towards freshwater, and remove the main environmental argument against them. As with many companies in today’s world, the shape of the narrative behind the technology carries an outsized influence on its ability to attract capital and talent to ultimately execute.

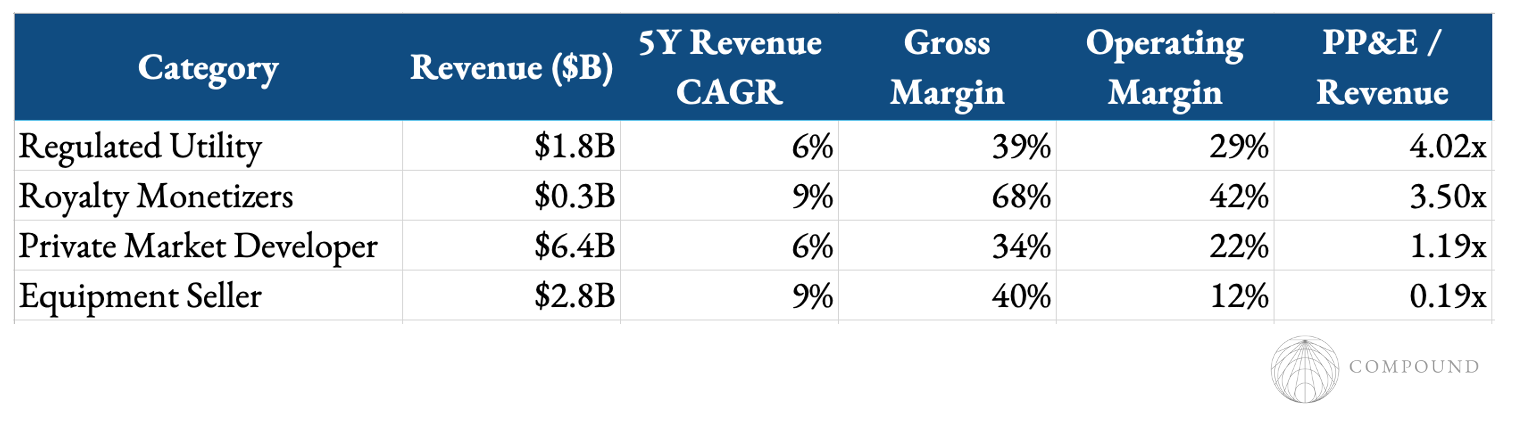

Finally, ideally companies in these spaces layer on top of their water processing tech an upcycling business model. While water is meant to be free, companies up and down its value chain have surprisingly decent businesses as seen below. However, augmenting its production with a second byproduct business line would make it all the more attractive. This type of layered sequencing is also important for attracting capital, especially given the limited venture-like outcomes in the water tech space historically. Though other upcycling examples exist, the top company to model the operations after is Safety-Kleen, which does $400M in revenue re-refining 150M gallons of oil annually into usable products. Such upcycling approaches require not just sophistication in technological development, but also in coordinating off-take agreement and ensuring high input flow rate for high plant utilization.

Who knows maybe some day even more creative business models like terraforming can be pursued if desalination and energy get cheap enough.

S/o to Smac for collaborating on this post